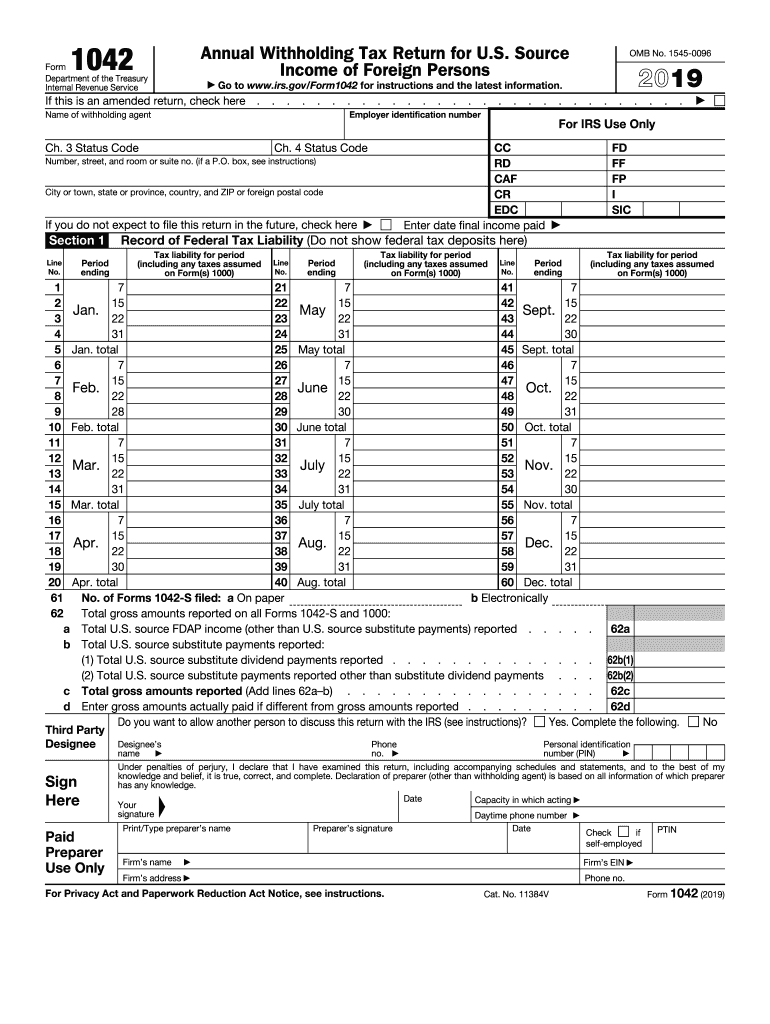

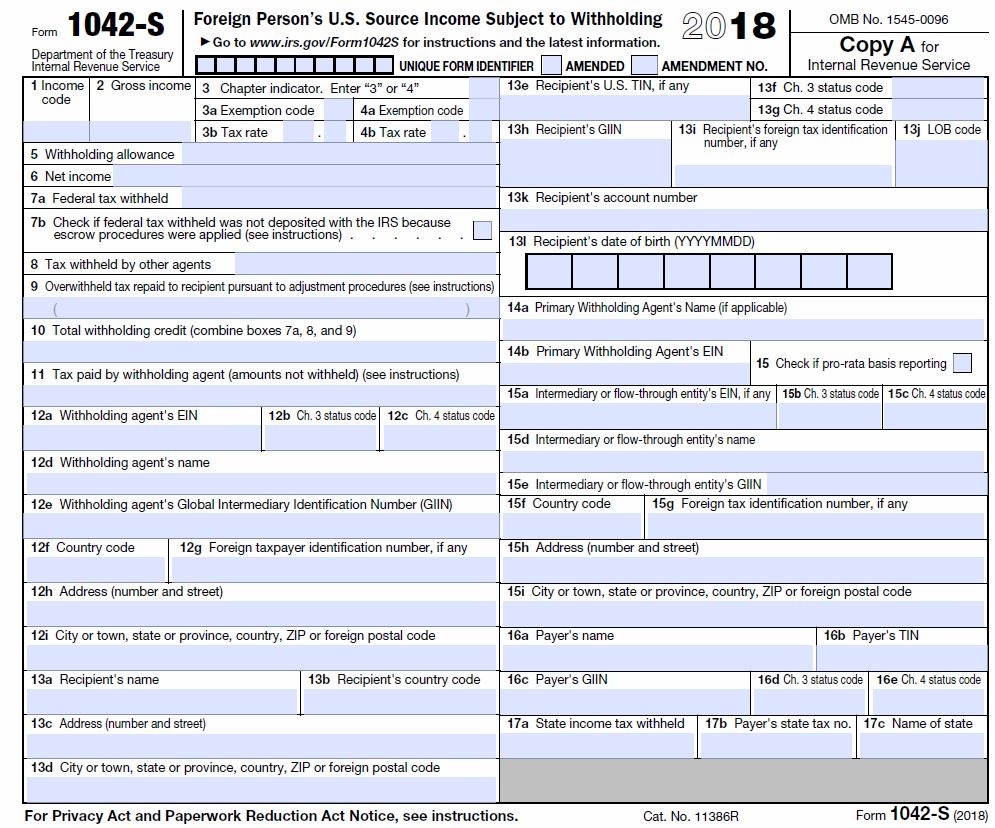

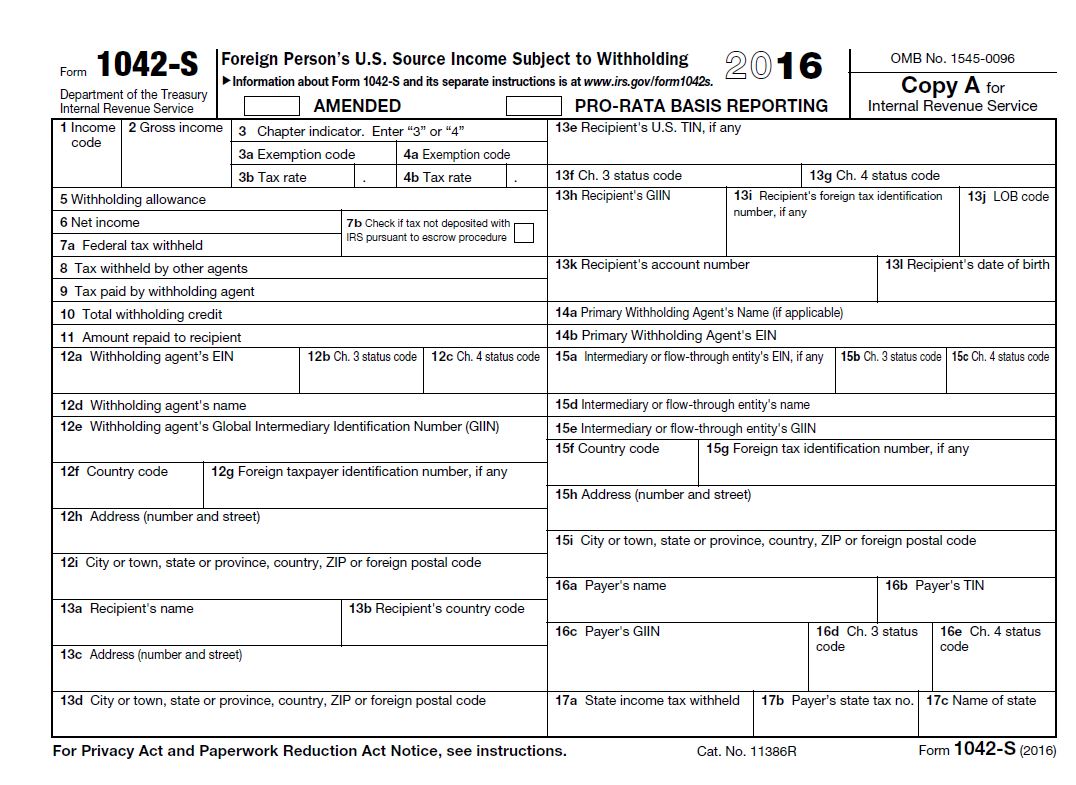

Form 1042 S

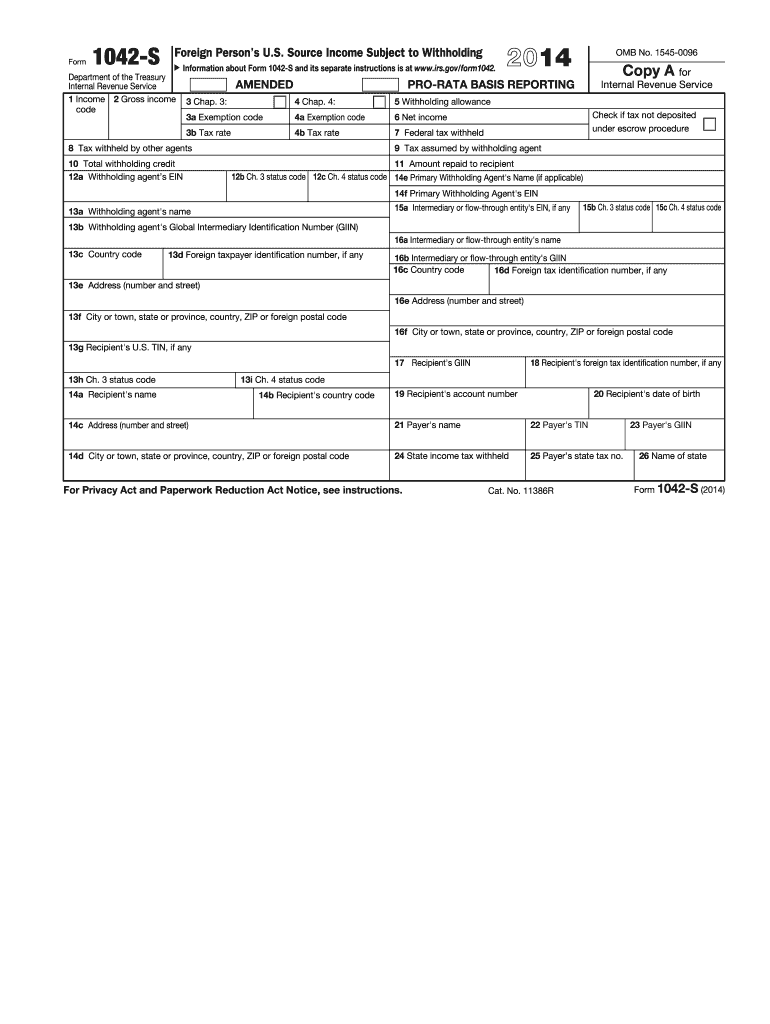

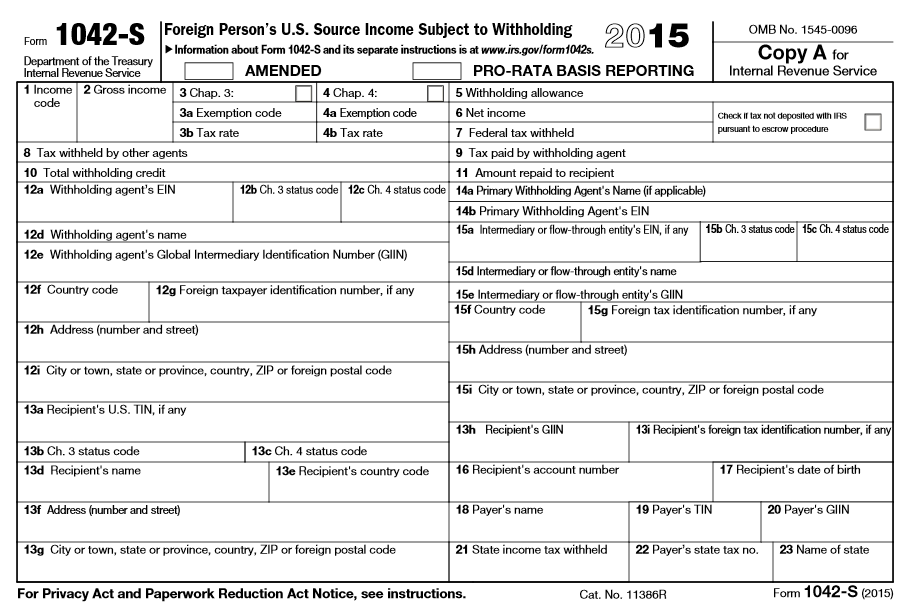

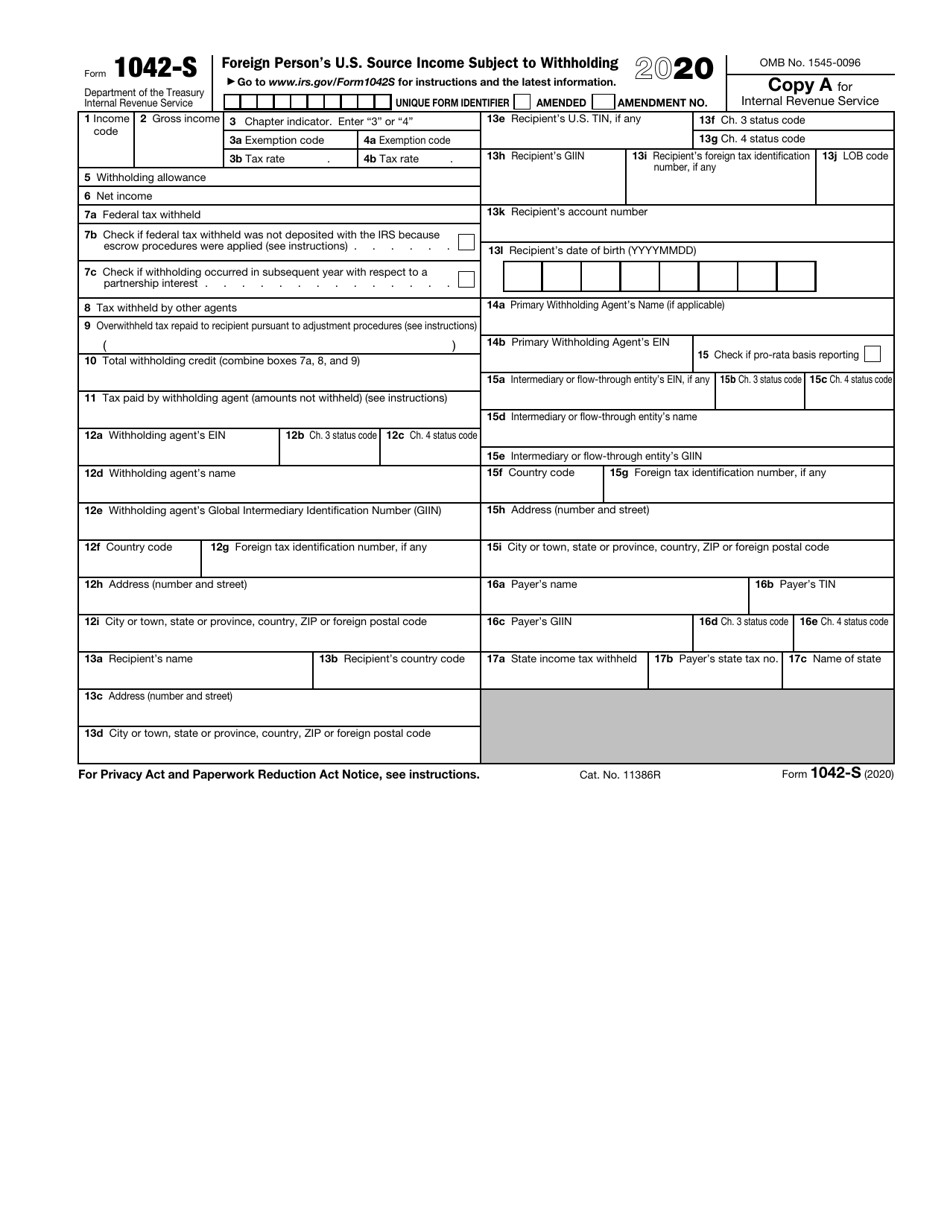

Form 1042 S - Source income subject to withholding, to report amounts paid to foreign persons that are described under amounts subject to nra withholding and reporting, even if withholding is not required on the payments. Source income subject to withholding, under the irc sections named above. Web use form 1042 to report the following. Income tax filing requirements generally, every nonresident alien individual, nonresident alien fiduciary, and foreign corporation with u.s. Amounts paid to foreign persons from u.s. Sources that are reportable under chapter 3 or 4 (regardless of whether withholding was required or not); Source income of foreign persons, including recent updates, related forms, and instructions on how to file. Source income subject to withholding, is used to report amounts paid to foreign persons (including those presumed to be foreign) by a united states based institution or business. Source income subject to withholding, is used to report any payments made to foreign persons. Income, including income that is effectively connected with the conduct of a trade or business in the united states, must file a u.s.

Income tax filing requirements generally, every nonresident alien individual, nonresident alien fiduciary, and foreign corporation with u.s. Web information about form 1042, annual withholding tax return for u.s. Web use form 1042 to report the following. Sources that are reportable under chapter 3 or 4 (regardless of whether withholding was required or not); Source income subject to withholding, to report amounts paid to foreign persons that are described under amounts subject to nra withholding and reporting, even if withholding is not required on the payments. Source income subject to withholding, under the irc sections named above. The tax withheld under chapter 3 (excluding withholding under sections 1445 and 1446 except as indicated below) on certain income of foreign persons, including nonresident aliens, foreign partnerships, foreign corporations, foreign estates, and foreign trusts. Source income subject to withholding, is used to report any payments made to foreign persons. Amounts paid to foreign persons from u.s. Use form 1042 to report tax withheld on certain income of foreign persons.

Source income subject to withholding, to report amounts paid to foreign persons that are described under amounts subject to nra withholding and reporting, even if withholding is not required on the payments. Income, including income that is effectively connected with the conduct of a trade or business in the united states, must file a u.s. Source income subject to withholding, including recent updates, related forms, and instructions on how to file. Web use form 1042 to report the following. The tax withheld under chapter 3 (excluding withholding under sections 1445 and 1446 except as indicated below) on certain income of foreign persons, including nonresident aliens, foreign partnerships, foreign corporations, foreign estates, and foreign trusts. Sources that are reportable under chapter 3 or 4 (regardless of whether withholding was required or not); Amounts paid to foreign persons from u.s. Income tax filing requirements generally, every nonresident alien individual, nonresident alien fiduciary, and foreign corporation with u.s. Source income of foreign persons, including recent updates, related forms, and instructions on how to file. Source income subject to withholding, under the irc sections named above.

2019 Form IRS 1042 Fill Online, Printable, Fillable, Blank pdfFiller

Source income subject to withholding, to report amounts paid to foreign persons that are described under amounts subject to nra withholding and reporting, even if withholding is not required on the payments. Web information about form 1042, annual withholding tax return for u.s. Use form 1042 to report tax withheld on certain income of foreign persons. The tax withheld under.

Form 1042 S Fill Out and Sign Printable PDF Template signNow

Source income subject to withholding, is used to report any payments made to foreign persons. Source income subject to withholding, under the irc sections named above. Web use form 1042 to report the following. Source income subject to withholding, to report amounts paid to foreign persons that are described under amounts subject to nra withholding and reporting, even if withholding.

Form 1042S Explained (Foreign Person's U.S. Source Subject to

Source income subject to withholding, is used to report amounts paid to foreign persons (including those presumed to be foreign) by a united states based institution or business. The tax withheld under chapter 3 (excluding withholding under sections 1445 and 1446 except as indicated below) on certain income of foreign persons, including nonresident aliens, foreign partnerships, foreign corporations, foreign estates,.

IRS Form 1042S Download Fillable PDF or Fill Online Foreign Person's U

Sources that are reportable under chapter 3 or 4 (regardless of whether withholding was required or not); Source income subject to withholding, under the irc sections named above. The tax withheld under chapter 3 (excluding withholding under sections 1445 and 1446 except as indicated below) on certain income of foreign persons, including nonresident aliens, foreign partnerships, foreign corporations, foreign estates,.

1042 S Form slideshare

Web information about form 1042, annual withholding tax return for u.s. Source income subject to withholding, under the irc sections named above. The tax withheld under chapter 3 (excluding withholding under sections 1445 and 1446 except as indicated below) on certain income of foreign persons, including nonresident aliens, foreign partnerships, foreign corporations, foreign estates, and foreign trusts. Sources that are.

Understanding your 1042S » Payroll Boston University

Amounts paid to foreign persons from u.s. The tax withheld under chapter 3 (excluding withholding under sections 1445 and 1446 except as indicated below) on certain income of foreign persons, including nonresident aliens, foreign partnerships, foreign corporations, foreign estates, and foreign trusts. Income tax filing requirements generally, every nonresident alien individual, nonresident alien fiduciary, and foreign corporation with u.s. Source.

form 1042s 2021 instructions Fill Online, Printable, Fillable Blank

Source income subject to withholding, to report amounts paid to foreign persons that are described under amounts subject to nra withholding and reporting, even if withholding is not required on the payments. Source income subject to withholding, is used to report any payments made to foreign persons. Use form 1042 to report tax withheld on certain income of foreign persons..

1042 S Form slideshare

Sources that are reportable under chapter 3 or 4 (regardless of whether withholding was required or not); Amounts paid to foreign persons from u.s. Source income subject to withholding, is used to report any payments made to foreign persons. Source income subject to withholding, including recent updates, related forms, and instructions on how to file. Income, including income that is.

The Tax Times The Newly Issued Form 1042S Foreign Person's U.S

Source income of foreign persons, including recent updates, related forms, and instructions on how to file. Source income subject to withholding, is used to report any payments made to foreign persons. Use form 1042 to report tax withheld on certain income of foreign persons. The tax withheld under chapter 3 (excluding withholding under sections 1445 and 1446 except as indicated.

Form 1042S USEReady

Source income subject to withholding, is used to report amounts paid to foreign persons (including those presumed to be foreign) by a united states based institution or business. Use form 1042 to report tax withheld on certain income of foreign persons. Income tax filing requirements generally, every nonresident alien individual, nonresident alien fiduciary, and foreign corporation with u.s. Source income.

Web Information About Form 1042, Annual Withholding Tax Return For U.s.

Source income of foreign persons, including recent updates, related forms, and instructions on how to file. Use form 1042 to report tax withheld on certain income of foreign persons. Source income subject to withholding, is used to report amounts paid to foreign persons (including those presumed to be foreign) by a united states based institution or business. Income, including income that is effectively connected with the conduct of a trade or business in the united states, must file a u.s.

Source Income Subject To Withholding, Under The Irc Sections Named Above.

The tax withheld under chapter 3 (excluding withholding under sections 1445 and 1446 except as indicated below) on certain income of foreign persons, including nonresident aliens, foreign partnerships, foreign corporations, foreign estates, and foreign trusts. Source income subject to withholding, to report amounts paid to foreign persons that are described under amounts subject to nra withholding and reporting, even if withholding is not required on the payments. Source income subject to withholding, including recent updates, related forms, and instructions on how to file. Income tax filing requirements generally, every nonresident alien individual, nonresident alien fiduciary, and foreign corporation with u.s.

Web Use Form 1042 To Report The Following.

Amounts paid to foreign persons from u.s. Sources that are reportable under chapter 3 or 4 (regardless of whether withholding was required or not); Source income subject to withholding, is used to report any payments made to foreign persons.