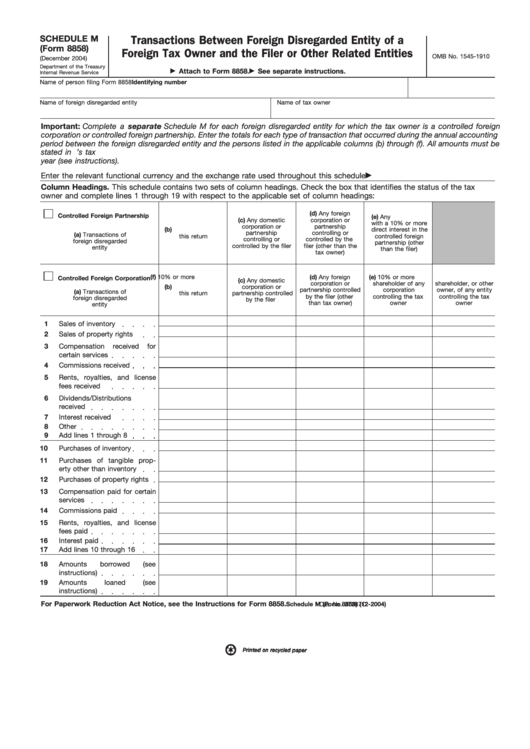

Form 8858 Schedule M

Form 8858 Schedule M - Person that is a tax owner of an fde or operates an fb at any time during the u.s. Web form 8858, schedule m, transactions between foreign disregarded entity of a foreign tax owner and the filer or other related entities. Go to www.irs.gov/form8858 for instructions and the latest information. Web schedule m (form 8858) (rev. Due to the many new schedules, filers will need to request information similar in scope to the form 5471 information request. Web complete the entire form 8858 and the separate schedule m (form 8858). Persons that own a foreign disregarded entity (fde) directly or, in certain circumstances, indirectly or constructively to satisfy the reporting requirements of sections 6011, 6012, 6031, and 6038, and related regulations. Web download or print the 2022 federal 8858 (schedule m) (transactions between foreign disregarded entity of a foreign tax owner and the filer or other related entities) for free from the federal internal revenue service. Transactions between foreign disregarded entity of a foreign tax owner and the filer or other related entities. Web all true foreign branches are now required to file form 8858.

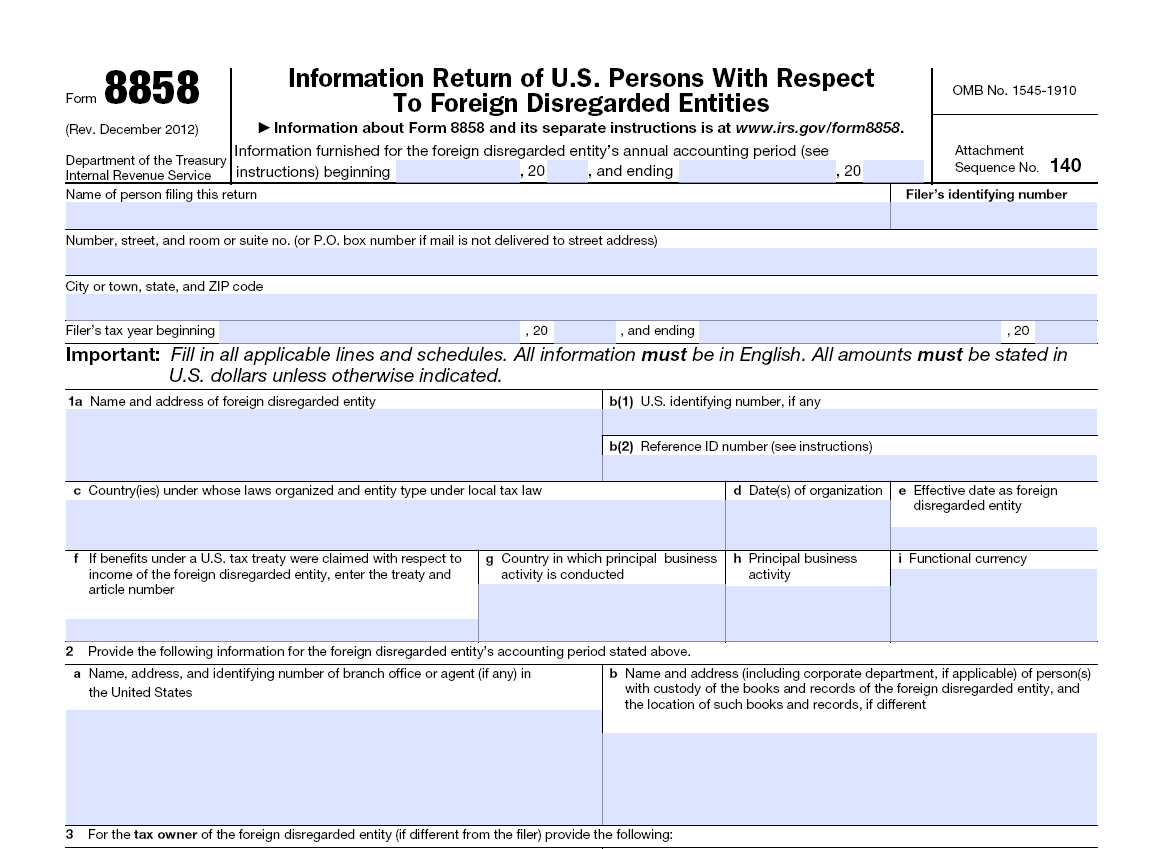

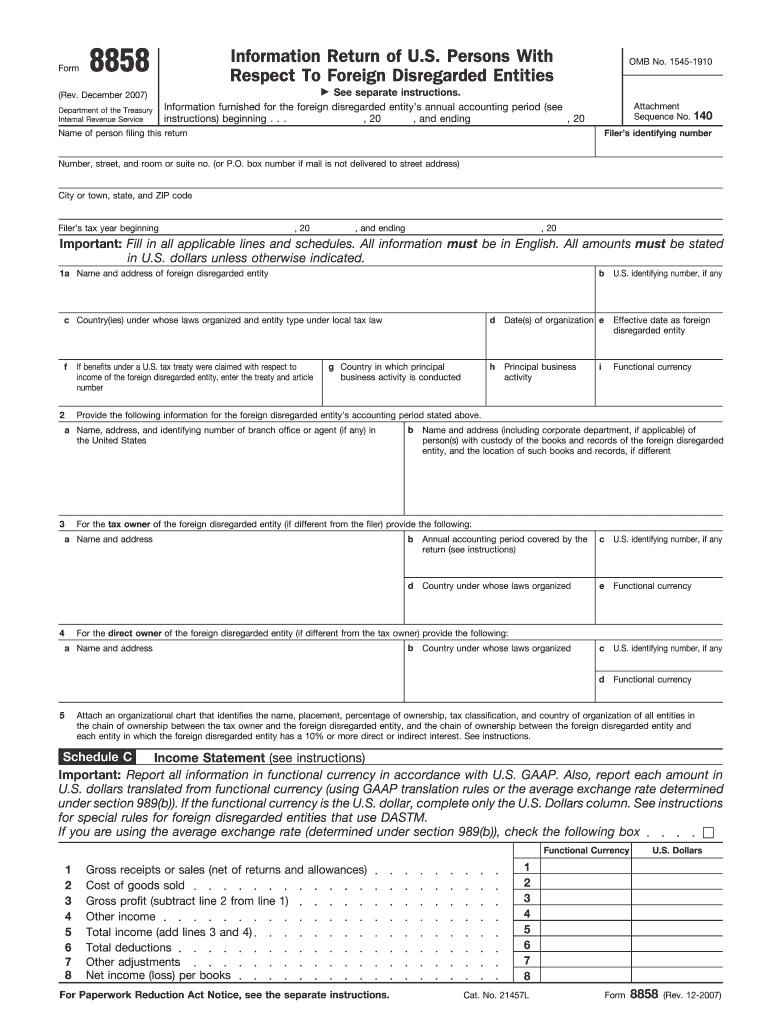

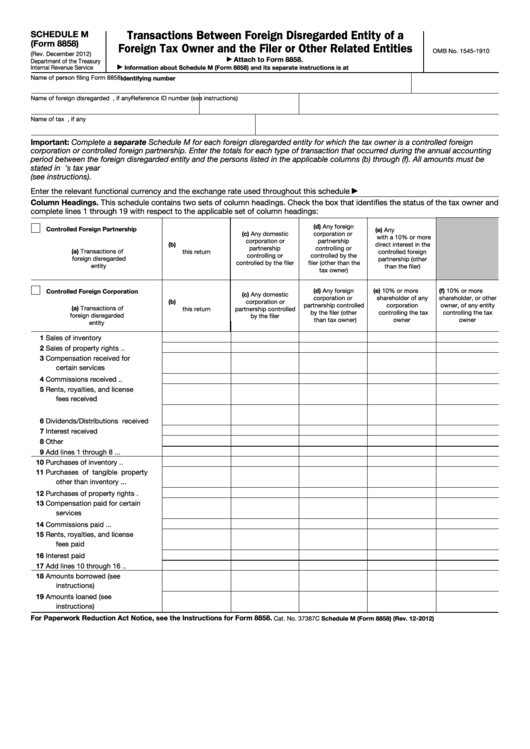

Due to the many new schedules, filers will need to request information similar in scope to the form 5471 information request. Web form 8858 is used by certain u.s. Person's tax year or annual accounting period. Persons that own a foreign disregarded entity (fde) directly or, in certain circumstances, indirectly or constructively to satisfy the reporting requirements of sections 6011, 6012, 6031, and 6038, and related regulations. Web form 8858, schedule m, transactions between foreign disregarded entity of a foreign tax owner and the filer or other related entities. December 2012) department of the treasury internal revenue service. Web fdes or fbs must file form 8858 and schedule m (form 8858). Go to www.irs.gov/form8858 for instructions and the latest information. Complete the entire form 8858, including the separate schedule m (form 8858), transactions between foreign disregarded entity (fde) or foreign Complete only the identifying information on page 1 of form 8858 (for example, everything above schedule c) and schedules g, h, j, and the separate schedule m (form 8858).

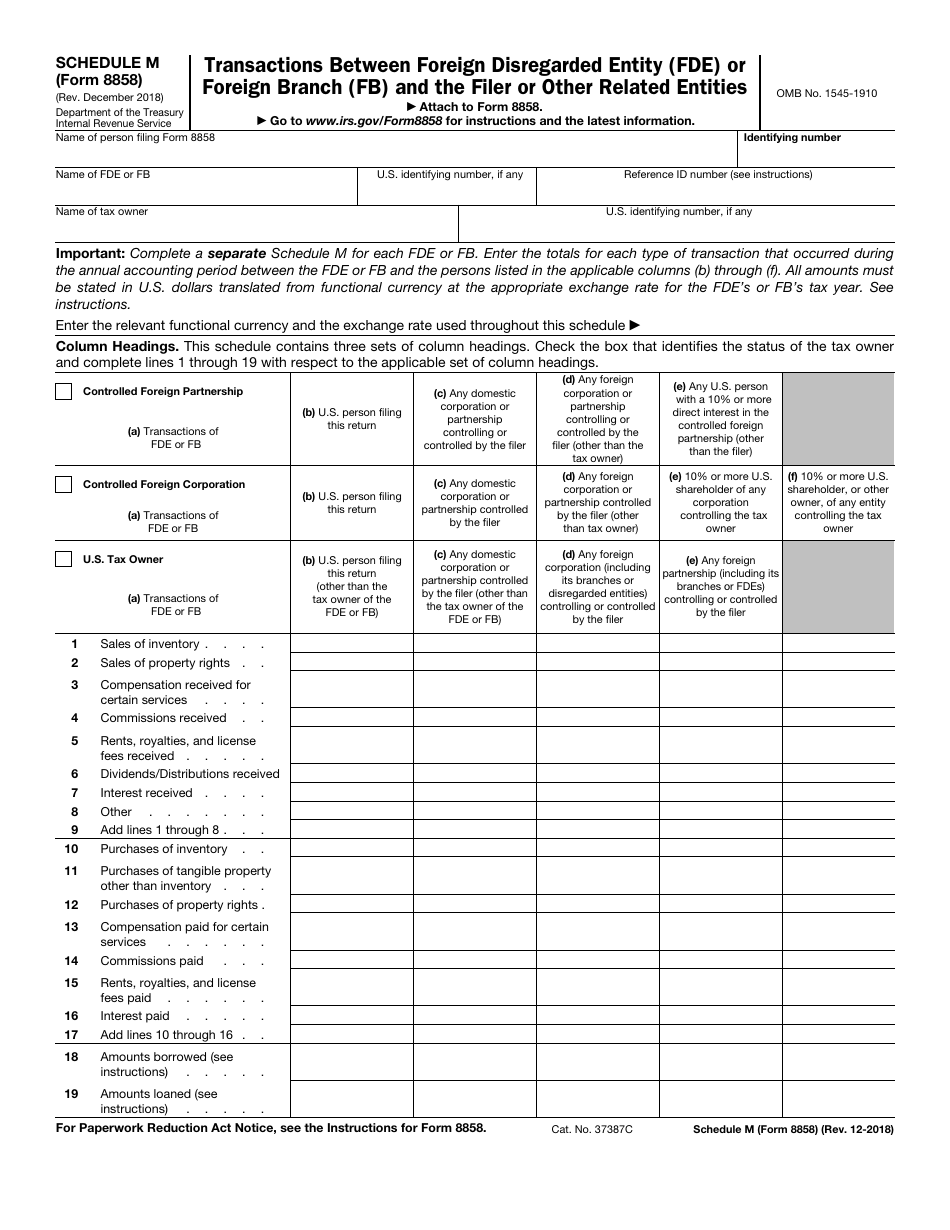

September 2021) transactions between foreign disregarded entity (fde) or foreign branch (fb) and the filer or other related entities department of the treasury internal revenue service attach to form 8858. Web schedule m (form 8858) (rev. Complete the entire form 8858, including the separate schedule m (form 8858), transactions between foreign disregarded entity (fde) or foreign Web download or print the 2022 federal 8858 (schedule m) (transactions between foreign disregarded entity of a foreign tax owner and the filer or other related entities) for free from the federal internal revenue service. Web schedule m (form 8858) (rev. Web all true foreign branches are now required to file form 8858. Category 2 filers of form 8865. Go to www.irs.gov/form8858 for instructions and the latest information. Person that is a tax owner of an fde or operates an fb at any time during the u.s. Persons that own a foreign disregarded entity (fde) directly or, in certain circumstances, indirectly or constructively to satisfy the reporting requirements of sections 6011, 6012, 6031, and 6038, and related regulations.

US Expat Tax Compliance Foreign Disregarded EntitiesUS Expat Tax

Web fdes or fbs must file form 8858 and schedule m (form 8858). Information about schedule m (form 8858) and its separate instructions is at. Complete the entire form 8858, including the separate schedule m (form 8858), transactions between foreign disregarded entity (fde) or foreign Persons that own a foreign disregarded entity (fde) directly or, in certain circumstances, indirectly or.

Form 8858 Fill Out and Sign Printable PDF Template signNow

Due to the many new schedules, filers will need to request information similar in scope to the form 5471 information request. Category 2 filers of form 8865. Go to www.irs.gov/form8858 for instructions and the latest information. Prior to tax year 2018, only us. Complete only the identifying information on page 1 of form 8858 (for example, everything above schedule c).

Form 8858 Information Return of U.S. Persons With Respect to Foreign

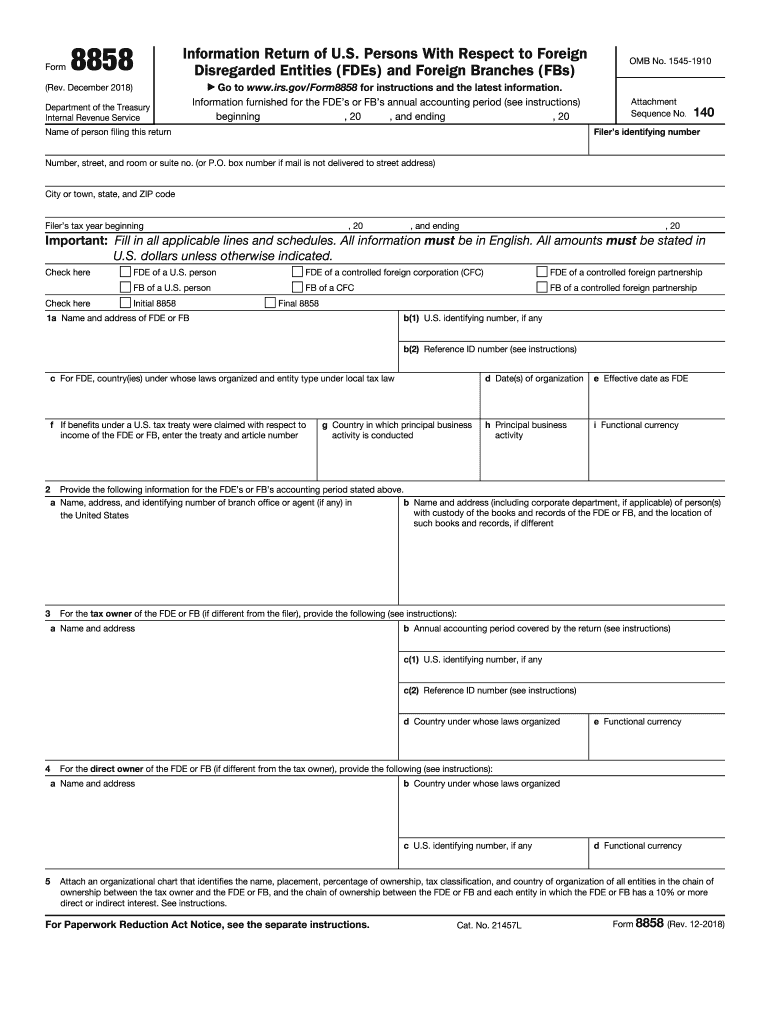

Persons with respect to foreign disregarded entities (fdes) and foreign branches (fbs). Category 2 filers of form 8865. December 2012) department of the treasury internal revenue service. September 2021) department of the treasury internal revenue service. Web all true foreign branches are now required to file form 8858.

Form 8858 (Schedule M) Transactions between Foreign Disregarded

Prior to tax year 2018, only us. Person that is a tax owner of an fde or operates an fb at any time during the u.s. Person's tax year or annual accounting period. Schedule m must be filed with form 8858 to disclose certain transactions between the fde and its tax owner. Category 2 filers of form 8865.

Form 8858 (Schedule M) Transactions between Foreign Disregarded

Person's tax year or annual accounting period. Go to www.irs.gov/form8858 for instructions and the latest information. September 2021) department of the treasury internal revenue service. Web schedule m (form 8858) (rev. September 2021) transactions between foreign disregarded entity (fde) or foreign branch (fb) and the filer or other related entities department of the treasury internal revenue service attach to form.

Fillable Schedule M (Form 8858) Transactions Between Foreign

Due to the many new schedules, filers will need to request information similar in scope to the form 5471 information request. Schedule m must be filed with form 8858 to disclose certain transactions between the fde and its tax owner. Information about schedule m (form 8858) and its separate instructions is at. Persons that own a foreign disregarded entity (fde).

Fill Free fillable F8858sm Schedule M (Form 8858) (Rev. December 2018

Web complete the entire form 8858 and the separate schedule m (form 8858). Person's tax year or annual accounting period. Schedule m must be filed with form 8858 to disclose certain transactions between the fde and its tax owner. September 2021) transactions between foreign disregarded entity (fde) or foreign branch (fb) and the filer or other related entities department of.

8858 Fill Out and Sign Printable PDF Template signNow

Go to www.irs.gov/form8858 for instructions and the latest information. Web all true foreign branches are now required to file form 8858. Web form 8858 is used by certain u.s. Complete the entire form 8858, including the separate schedule m (form 8858), transactions between foreign disregarded entity (fde) or foreign Persons that own a foreign disregarded entity (fde) directly or, in.

IRS Form 8858 Schedule M Download Fillable PDF or Fill Online

Transactions between foreign disregarded entity of a foreign tax owner and the filer or other related entities. Complete the entire form 8858, including the separate schedule m (form 8858), transactions between foreign disregarded entity (fde) or foreign Information about schedule m (form 8858) and its separate instructions is at. Due to the many new schedules, filers will need to request.

Fillable Form 8858 Schedule M Transactions Between Foreign

Web download or print the 2022 federal 8858 (schedule m) (transactions between foreign disregarded entity of a foreign tax owner and the filer or other related entities) for free from the federal internal revenue service. Persons that operate a foreign branch or that own (directly or indirectly, through a tier of foreign disregarded entities or partnerships) certain interests in foreign.

Go To Www.irs.gov/Form8858 For Instructions And The Latest Information.

Person's tax year or annual accounting period. Web fdes or fbs must file form 8858 and schedule m (form 8858). Web schedule m (form 8858) (rev. Web download or print the 2022 federal 8858 (schedule m) (transactions between foreign disregarded entity of a foreign tax owner and the filer or other related entities) for free from the federal internal revenue service.

Category 2 Filers Of Form 8865.

September 2021) transactions between foreign disregarded entity (fde) or foreign branch (fb) and the filer or other related entities department of the treasury internal revenue service attach to form 8858. Web schedule m (form 8858) (rev. Persons that operate a foreign branch or that own (directly or indirectly, through a tier of foreign disregarded entities or partnerships) certain interests in foreign tax owners of foreign branches must now file form 8858 and schedule m, transactions between foreign disregarded entity (fde) or foreign branch (fb) and the filer or other. December 2012) department of the treasury internal revenue service.

Complete Only The Identifying Information On Page 1 Of Form 8858 (For Example, Everything Above Schedule C) And Schedules G, H, J, And The Separate Schedule M (Form 8858).

Web all true foreign branches are now required to file form 8858. September 2021) department of the treasury internal revenue service. Prior to tax year 2018, only us. Schedule m must be filed with form 8858 to disclose certain transactions between the fde and its tax owner.

Transactions Between Foreign Disregarded Entity Of A Foreign Tax Owner And The Filer Or Other Related Entities.

Persons with respect to foreign disregarded entities (fdes) and foreign branches (fbs). Persons that own a foreign disregarded entity (fde) directly or, in certain circumstances, indirectly or constructively to satisfy the reporting requirements of sections 6011, 6012, 6031, and 6038, and related regulations. Web form 8858 is used by certain u.s. Web form 8858, schedule m, transactions between foreign disregarded entity of a foreign tax owner and the filer or other related entities.